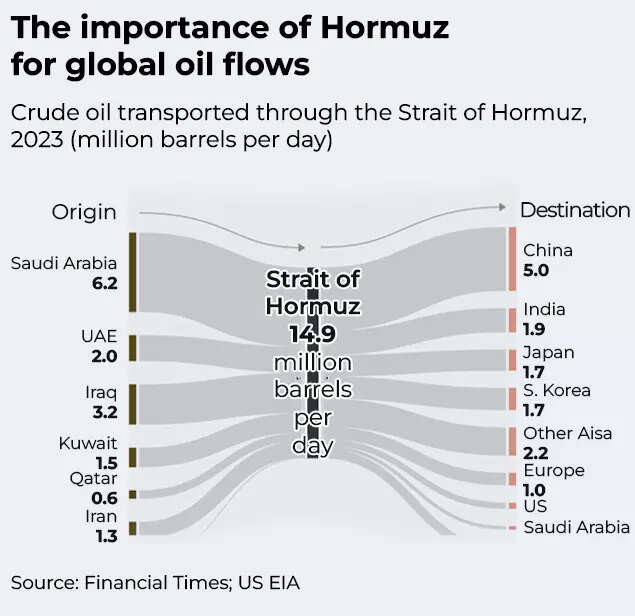

Inflation at a benign 2.2% and growth at 8.0% in the first half of 2025-26 present a rare goldilocks period – that’s what RBI governor Sanjay Malhotra said in the central bank’s December monetary policy review. Three months later, India’s economy – the world’s fastest growing major economy – faces the prospect of slipping out of this golden period – its high growth may be hit by the economic fallout from the ongoing war, and rising oil prices may mean higher inflation soon. This is not to say that India’s long-term growth story is not intact. Economists believe that GDP growth may take a hit of around 30-50 basis points, and inflation may rise in the short-term.The US-Israel-Iran war has dealt a crude blow to the world economy in the form of oil prices rising above $100 per barrel. The entire Middle East has been engulfed in the conflict, choking the Strait of Hormuz from which key oil and trade supplies get routed. Middle East countries are also important exporters of crude oil, and with refineries coming under attack, oil supply globally may see an unprecedented hit. Iran has even warned that oil prices may hit $200 levels if the conflict doesn’t see a resolution soon.What does this mean for us back home? India is among the world’s largest importers of crude oil, meeting around 90% of its needs through imports. A big chunk of these supplies come from Middle East countries and make their way to Asia through the Strait of Hormuz. The vulnerability is not just limited to oil – LPG and LNG supplies which feed into household and industrial needs have also been curtailed.

What do rising crude oil prices spell for India’s GDP growth, inflation, current account deficit, rupee, and fiscal deficit? Economists say that the answer lies in the length of the war. The persistence and sustainability of high oil prices will play a key role in shaping the scale of the economic impact on countries.

Current Account Deficit Under Pressure

The most immediate hit to the economy comes in the form of current account deficit (CAD) widening. Current account deficit happens when the value of imports into a country is more than the exports, implying that it spends more foreign currency than it earns.With oil prices rising the crude import bill will go up – which in turn will feed into a rising CAD. Economists believe that if oil prices stay above $100, it would deal a blow to the balance of payments.Madan Sabnavis, Chief economist at Bank of Baroda estimates that CAD will be affected by $18 bn for every $10 increase in price of oil. “This is the direct impact. Exports of refinery products also get directed to the Gulf region which can take a hit. Further, prolonged war can affect the entire dynamics of global trade. Add to this the fact that remittances from the GCC countries can get affected due to the ongoing conflict and the potential hit to the CAD can be 0.5-0.75% of GDP,” he cautions.Sujan Hajra, Chief Economist & Executive Director, Anand Rathi Group that in case of persistently high levels of oil, the CAD would rise. “For a large, persistent move, CAD can rise by roughly 0.4 percentage points of GDP for every $10 increase in oil, other things equal. Therefore, from the pre-war level of $70/barrel, if crude oil prices remain at $100/barrel on a sustained basis, India’s CAD would increase by 1.2% point of GDP and reach 2.5-2.7% of GDP,” he tells TOI.Ranen Banerjee, Partner and Leader, Economic Advisory Services, PwC India sees a drain on foreign exchange if oil prices continue to rise. “A sustained increase in oil prices would cause a serious drain on forex and consequently the current account deficit. The situation is exacerbated as the underlying cause for higher oil prices is conflict and by deduction, if the conflict continues longer then it will impact both goods and services exports as well as investment climate,” he tells TOI.“This will have an adverse impact on remittances, portfolio flows and FDI and that would further stress the exchange rate. The imports will thus become more expensive in rupee terms adding imported inflation in the economy,” he explains.Radhika Rao, Senior Economist, DBS Bank notes that encouragingly, the economy’s oil intensity has reduced from the past, as signaled by the moderation in the net oil imports. However, she points out that with the Middle East region making up approximately 40% of total remittances, inflows balance of payments faces a second order impact if the conflict prolongs.

Rupee: No Respite From Depreciation

The Indian rupee had a bad 2025, with the currency being the worst performer in Asia. 2026 is not turning out to be any better, and the Middle East tensions have added to the pressure. From an economics standpoint, a wider CAD, higher imported inflation and risk off sentiment usually mean a weaker rupee.“The currency tends to depreciate more if oil stays high and capital flows soften, although forex reserves and occasional intervention can smooth the move,” says Sujan Hajra. The expert doesn’t expect the rupee to depreciate more than 2-3%, unless the situation deteriorates significantly.Madan Sabnavis acknowledges that the rupee will tend to be under pressure and can depreciate depending on the dollar index and intervention by the RBI. As of now Rs 91.5-93 is the short-term forecast till March end, he says.

Inflation: How Long Can Prices Be Kept Stable?

Fundamentally, if the cost of imports goes up – whether due to rising prices internationally (such as in the case of oil), or due to depreciating rupee, it all feeds into prices of goods and services going up. India has seen a period of benign inflation for some quarters now – but now with oil prices skyrocketing, this math will change.For Madan Sabnavis, the impact on WPI inflation is straightforward. “10% increase in fuel prices leads to WPI going up by 1%. Add another 0.5% as secondary impact and it will be up by 1.5%. CPI will depend a lot on how the government deals with the fuel prices. In extreme cases, the prices at pump may rise by Rs 2-3/litre which combined with higher LPG prices as well as other consumer products like paints, chemicals, etc. can add 0.5% to CPI,” he tells TOI.

")

CPI inflation trajectory (Source: EY India)

Experts point to two important aspects of the situation: one – how long will the conflict last? Secondly, will the government pass on the increase in oil prices to consumers or absorb the shock?Radhika Rao of DBS Bank says, “The extent of impact on inflation will be dictated by who picks the incremental cost burden. India had undertaken measures to reform its fuel sector by deregulating petrol and diesel prices, allowing them to align with market rates to reduce fiscal deficits and losses of the upstream oil marketing companies. This helped to lower the fiscal burden on the government’s books, with total subsidies accounting to 1.2-1.3% of GDP, of which petroleum is almost negligible at less than 3% of the total. However, in the event of a sharp rise in global fuel prices, authorities are likely to be cautious about fully passing on higher costs to consumers.”The need to protect household purchasing power and support businesses as well as a packed state election calendar in the first half of 2026 may prompt a more measured approach to retail fuel price adjustments, with the initial rise likely to be absorbed by the oil marketing companies. As an alternative to raising retail prices, excise duty cuts might be considered,” she tells TOI.With full pass-through of higher crude feeds into fuel, transport and input costs, Sujan Hajra says that retail inflation increases by roughly 25 basis points for every 10 dollar sustained increase in oil prices. Therefore, sustained increase in crude oil prices by $30/barrel (from $70 to $100) can increase inflation by 75 basis points, he says, adding that the government is unlikely to implement a full pass-through. With even 50% pass-through the impact on retail inflation would be around 40 basis points, he forecasts.But, for how long can the oil shock be absorbed if the conflict continues? Ranen Banerjee explains that while the oil companies have a buffer to hold the pump prices at current level for some time, the pressure on the fiscal owing to the same cannot be sustained if oil remains above $100 a barrel.“The fertiliser subsidy will go up as fertiliser prices will be higher. With consequent increase in food inflation, food subsidy requirements will also go up,” he says.

Fiscal Deficit And Management Under Strain

In a developing economy like India, managing fiscal math is a challenge every year, and the situation has been exacerbated by the oil shock. How does this happen? The fiscal gets affected by subsidy bills going up, non-tax revenue coming down as OMCs will not be able to transfer the same quantum of profit, excise collections coming down in case excise is lowered by the centre to keep petrol, diesel prices the same. Sourav Mitra, Partner – Oil & Gas at Grant Thornton Bharat elaborates on the channel through which higher oil prices feed into the economy.Elevated oil prices increase the cost of fertilizer, LPG, and kerosene subsidies, as the government often absorbs part of the price shock to protect end consumers. The central government’s expenditure could significantly increase, primarily due to higher fertilizer subsidies, he tells TOI. “Higher crude prices also constrain the government’s revenue sources, particularly on fuel taxation. While excise duties on petrol and diesel are a key revenue source, the ability to raise fuel taxes goes away when global prices rise sharply, limiting fiscal flexibility. The government may even be forced to cut excise duties to control inflation, leading to revenue losses. Combined with slower economic growth and higher borrowing needs, this can push the fiscal deficit above budgeted targets, increase public debt, and crowd out private investment,” he says.Sujan Hajra tells TOI, “If the government absorbs part of the shock via lower excise or higher subsidies, the fiscal deficit and borrowing needs widen and fiscal consolidation can get delayed. Higher inflation can also keep interest rates higher for longer, pushing up government interest costs.”However Madan Sabnavis believes that the fiscal deficit will be maintained as other expenses can be fine-tuned. At most the impact can be 0.1-0.2% of GDP, he says.

GDP: Blow To Growth Story?

Economists and experts warn that a prolonged war-like situation would weigh on India’s growth story, impacting several sectors and the growth momentum.“The impact on the economy in a scenario where conflict drags longer will have several levels of adverse impact and would impact our growth rate too. In a scenario where conflict is resolved in a short time frame, we should not expect much impact. However, if the duration stretches to a quarter, then we should expect a 50-75 bps downward impact on growth,” says PwC India’s Ranen Banerjee.“Any continuation beyond that time frame will cause disruptions of a magnitude that the global economy could possibly not afford and hence is a very pessimistic scenario,” he adds. Sujan Hajra points out that India is more vulnerable than net oil exporters like the US or some West Asian economies, and somewhat more exposed than many advanced economies, but broadly comparable to other large, oil‑importing emerging markets; strong services exports and remittances provide a partial cushion.“The rule‑of‑thumb estimates suggest every $10 sustained rise in crude can shave about 0.4 percentage points off India’s real GDP growth through weaker consumption, higher input costs and tighter monetary policy. Therefore, under the current situation, India’s growth could go down to around 6-6.5% versus earlier expectations of 7-7.5%. This, however, assumes continuation of the conflict at the current intensity for a prolonged period,” he tells TOI.Madan Sabnavis of Bank of Baroda is more optimistic about India’s prospects, predicting that the economy may still manage a 7% GDP growth rate.“GDP impact will be limited and a hit of 0.1-0.2% can be a possibility due to supply disruptions and higher prices of oil – which come in as higher input costs for user industries. Growth can be closer to 7% than 7.5%,” he says.High oil prices is a nightmare scenario for most of the global economy – and India is no different. The impact on major economic indicators, especially GDP growth and inflation may be contained in the short-term. India’s potential of 7% GDP growth and inflation within RBI’s target range may well still be achievable in the upcoming financial year.But, a medium to long-term continuation of the conflict would have more widespread consequences.As Ranen Banerjee of PwC India concludes: India will be impacted significantly as any other economy in the world and the only extra cushion we would have is the large domestic consumption base. But private consumption will also be challenged in a disrupted scenario that lasts longer than a quarter. “The ensuing panic and uncertainty would lead to consumption deferral for non-essentials and thus impact almost all sectors negatively,” he says.